Billing

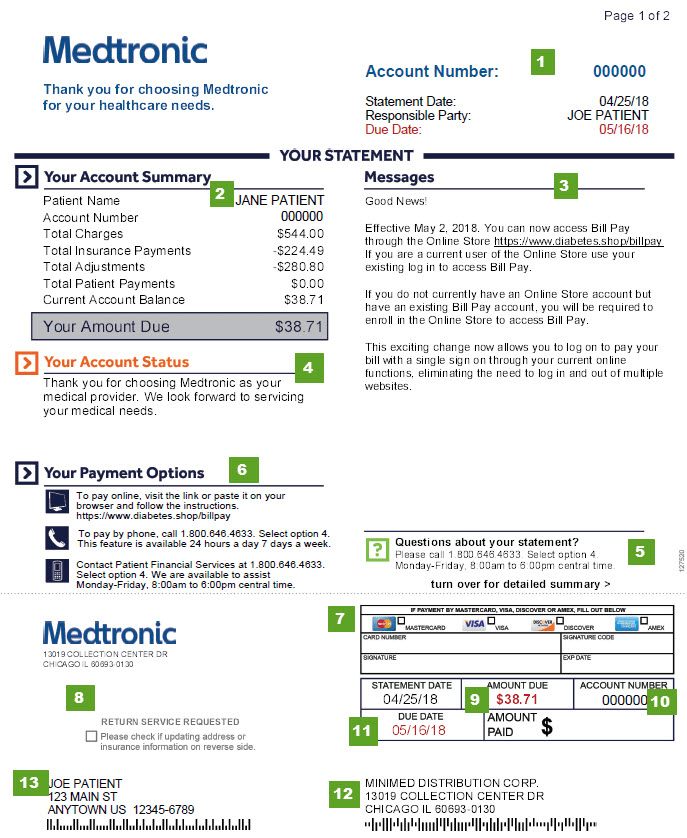

- Date the statement was printed

- Summary of your account balance

- Important messages and reminders

- The status of your account

- Contact the Patient Financial Services Team at 1-800-646-4633, select option 4

- Your payment options

- Area to complete if paying by debit or credit card

- Check this box if providing updated address or insurance information on the back

- Total amount due including any previously unpaid balances

- Your unique Medtronic identification number

- Date payment is due

- Make checks payable to "MiniMed Distribution Corp." and mail to this address

- Name of person financially responsible

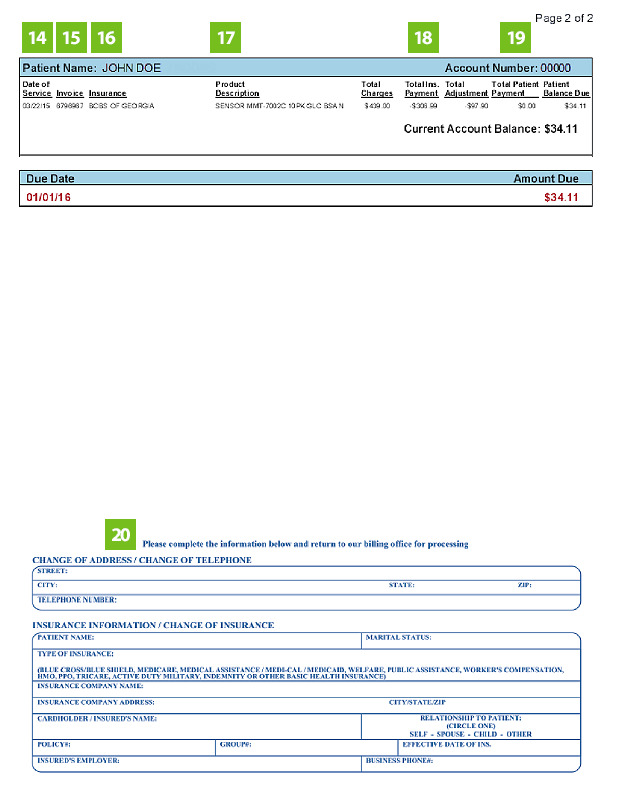

- The date for services provided

- The invoice number for a specific date of service

- The payer who was billed

- Items provided to you on a specific date of service

- Amount paid by your insurance for a particular claim or date of service

- Amount you have paid Medtronic for each individual claim or date of service

- Complete this section if you need to update any personal or insurance information.

Important: If updating information, check the box on the first page (Item 7)

Debit or credit card

Pay with a debit or credit card by following these steps:

- Fill in the required information in the Account Status section on your bill

- The type of card: Visa, MasterCard, Discover, or American Express

- Card number

- Signature code (the 3-digit security code listed on the back of your card)

- Signature

- Expiration date

- Tear off the bottom piece of the bill

- Put it in the envelope that came with your bill, making sure the address is visible in the clear window

Check or money order

- Make your check out to: MiniMed Distribution Corp. and send to the following address. Note that any correspondence related to your billing statement may also be received at this address.

- The mailing address is:

MiniMed Distribution Corp.

13019 Collection Center Drive

Chicago, IL 60693-0130

- The mailing address is:

- Also make sure to include your account number on the memo line of the check. Can't find your account number?

- If you don't have a copy of your billing statement, a Patient Financial Team Member can look it up for you Monday–Friday, 8 a.m.–6 p.m. CT at 1-800-646-4633 and select option 4.

Call us

Call a Patient Financial Team Member Monday–Friday, 8:00 a.m.–6:00 p.m. CT at 1-800-646-4633 and select option 4 to use a debit or credit card.

When you call, be prepared to provide:

- The type of card: Visa, MasterCard, Discover, or American Express

- Name on the card

- Expiration date

- Debit or credit card number

- Security code listed on the back of your card